This week: reasons for pessimism

A week after I told you some reasons to be optimistic

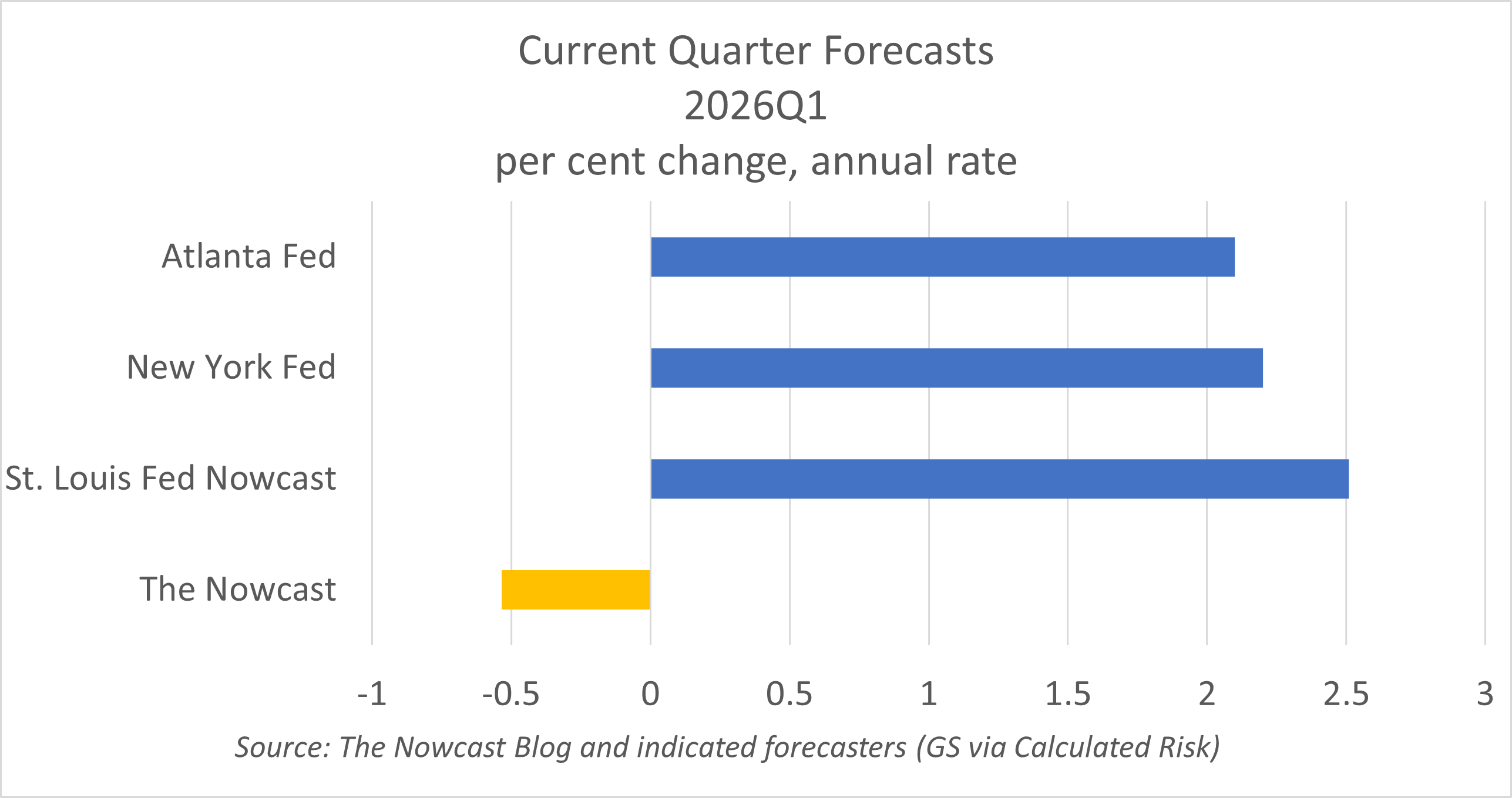

Last week, I stepped on my own model’s forecast by explaining why it was probably too pessimistic. This week’s unchanged model forecast (-0.5% real GDP growth in Q1) continues to exclude some important positive factors, like the snap back in government spending. But two things now make the case for pessimism stronger.

The employment release was a problem, no doubt. In particular, it wasn’t AI. The industry category that includes a large share of computer workers, Computer Systems Design and Related Services, gained 5,900 workers. The big losers were in Manufacturing, Construction, Transportation and Warehousing, and Leisure and Hospitality. (Health Care also lost workers, but that was mainly because of a strike). This looks more like a delayed reaction to tariffs than anything else. Of course, it’s only one month, but it’s the second really alarming release we’ve had (the first being December retail sales, which were negative in real terms).

The war in Iran: the initial economic impact is rather small, and the US is an oil exporter, on net, so in theory higher oil prices aren’t bad for the US economy. Tell that to consumers faced with higher gas prices. We know that gasoline prices play an unusual and overweighted role in consumer behavior. In a situation where consumer sentiment is already unusually low, the impact on spending may be significant enough to outweigh the extra profits from energy exports.

And to top it off, the Atlanta Fed’s GDPNow forecast was revised down from 3.2% to 2.1% this week.

Is a recession coming? Keep in mind that recessions are not caused by consumers pulling back spending. But a sustained stock price decline could uncover the type of risk mispricing that does lead to recessions. In a world of opaque private capital and crypto, such mispricing is very likely to be happening.

No to the consumer-led AI recession

The Nowcast’s Author being retired, I sometimes wait to comment on events. The recent Citrini report is one of those. By now, the frenzy it created has been replaced by headlines about drones in the Middle East, so maybe it’s a better time to sit down and think about the scenario outlined in the report.

The scenario seems quite unlikely. I see several reasons why things won’t unfold this way. (HT to my colleague Monali Samadar, who asked me about the report and so forced me to marshal my thoughts about it into coherence.)

There has never been a consumer-led recession. Recessions are created by the sudden discovery of risk mispricing or by oil shocks. (Or by pandemics, as we now know). That’s about it! So this story would be very much ahistorical. I always mistrust people who create science fiction that isn’t grounded in past human experience.

I think that the report really doesn’t take into account the speed at which new technology is adopted. People just don’t change how they do things that quickly, and systems and organizations change only gradually and reluctantly. It took US auto companies decades of losing market share to Japanese car companies before they changed how the operated. We aren’t suddenly going to all adopt AI agents at once!

Trust is a big deal, and will slow adoption a lot. It will probably take years before we trust these agents enough, especially for anything involving money or health. Which is a lot of stuff! This paper is my favorite still https://kfai-documents.s3.amazonaws.com/documents/c3cac5a2a7/AI-as-Normal-Technology---Narayanan---Kapoor.pdf. He points out that we don’t even trust older AI type technologies, like traditional statistical models, to operate without human intervention. Why would new “black box” technologies be any different? It will take time to trust (e.g.) the computer to even make travel plans for us. Trust is earned over time, which stretches out the adoption period of new technology

Even then, lots of white collar workers are immune. Ministers, Priests, and Rabbis, for example. (It’s a bizarre dream to think that these relationships will somehow be replaced in a short period of time by robots, if there is any possibility of their being replaced at all). Just because we economists find that certain skills can be done by AI doesn’t mean that people want AI to replace people in those areas. An example: how many of us still bristle at AI agents for customer service, and insist on talking to a “real person.” I don’t think that’s just a boomer thing!

Finally, the real issue isn’t AI taking jobs: it’s mispricing securities as the world changes. The real danger of fast AI adoption is that investments that appeared to be “safe” assets turn out to be risky, creating capital flight and sudden stops of lending. That has historically been the component that creates recessions, and it’s the component that we should expect is most likely to create the next recession. AI may flavor the recession, but the dynamics will be recognizable to a French investor in John Law’s Mississippi Company.