Some price data for March leaves the forecast unchanged

And The Nowcast is taking a vacation

This week’s forecast includes two price measures, which had small, but offsetting impacts on the forecast.

The producer price index increase was quite subdued, except for the impact of higher fuel prices. The result was a large increase in the PPI for goods, which the model uses as a proxy for the deflator for inventories. The result: the model now expects real inventories to be down $36 billion (compared to $15 billion last week).

Export and import prices were also up, oddly not just because of fuel. This was closer to the market’s expectations than the PPI for goods, but the forecasts for both real exports and real imports fell. The result was an increase in the forecast for net exports of about the same amount as the fall in the forecast for inventories.

The impact of price data in March (and possibly in February) is unreliable in this model. The problem, of course, is that a large increase in fuel prices can drive the overall price index, but it may not have a large an impact when placed in the context of all goods and services. In addition, the monthly inventory data used here doesn’t include all petroleum inventories, and that has, in the past, swung inventory data quite a bit when prices change. Plus, inventories themselves are likely being drawn down, perhaps without registering in the monthly data).

The overall message remains the same: the US economy was likely weakening before the oil shock from Iran. The price of oil doesn’t appear to have reacted as much as might have been expected, leaving room for oil prices to rise even more. And, despite the ceasefire, higher oil prices may be the case for quite some time, and perhaps even permanently, if we see a Hormuz tax put in place. The downsides for the US economy remain considerable.

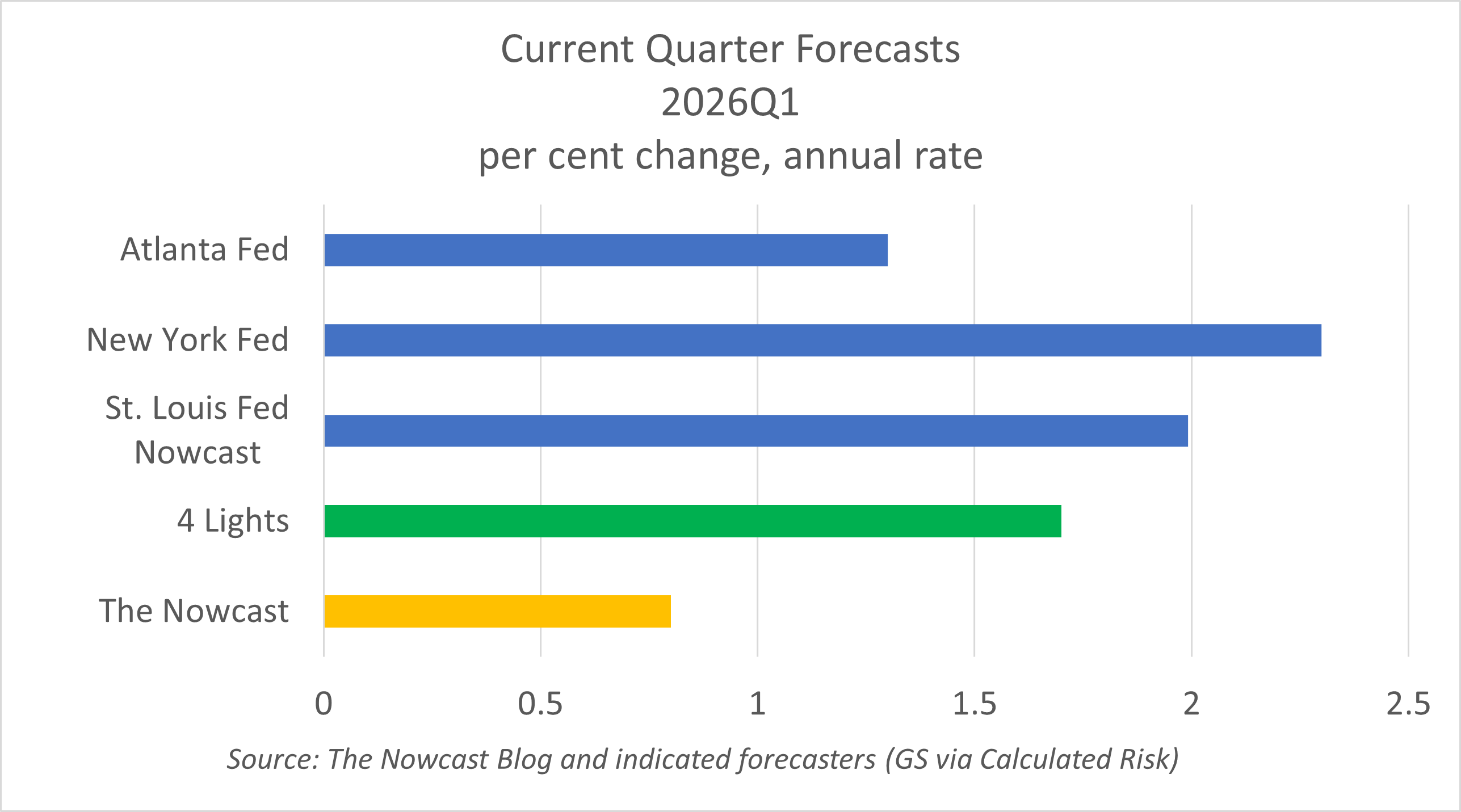

Like the Nowcast, Fed nowcasts were unchanged this week. Changes in the Polymarket prediction were also very small, although there may be a slight rise in optimism; notice the 4% rise in 2.0% to 2.5% growth (which looks high right now) and the slight fall in less than 1.0% growth—the Nowcast baseline.