New data points to another hot quarter

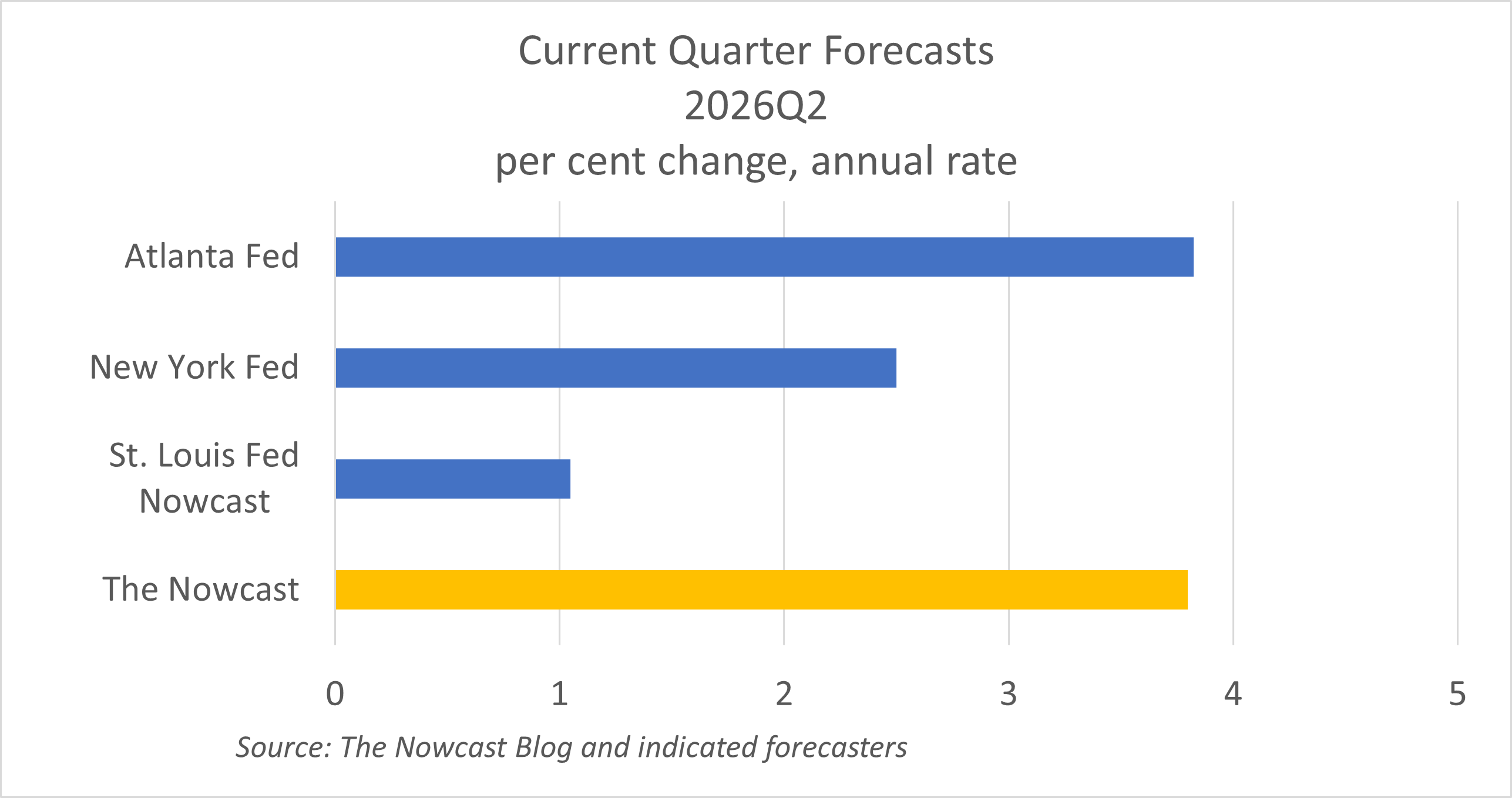

Advance trade data boosts Q2 GDP to 3.8%

It’s time to put aside the narrative of slowing growth yet again. Two releases in the past week boosted the Q2 forecast from 1.9% to 3.8%. That’s despite the downward revision to GDP. If the economy is really slowing, it’s not showing up in the data yet.

Real consumer spending was higher than forecast in April. BEA also revised real consumer spending up in March, which sets up Q2 for faster growth. The impact was surprisingly large because the revisions apply to the last month of the previous quarter, and the first month of this quarter. The “leap-off” effect leads to a forecast consumer spending growth to 2.1% for Q2, up from 1.7% last quarter, and a number that’s certainly consistent with a healthy economy.

All is not necessarily perfect when it comes to consumer spending. Over the past year, spending growth has far outpaced income growth, and the saving rate has halved (from 5.5% last April to 2.6% in the latest data). That can’t continue. Either spending will eventually slow, or incomes will pick up.

It all depends—as always—on whether the labor market continues to deliver job growth. But job growth so far has been strong, and that helps to anchor consumer spending.

The initial data on international trade (Advance Report on International Trade) changed the trade picture quite a bit. It suggested that strong export growth will be accompanied by a slight decline in imports in April. The model now estimates that real international trade will improve by $86 billion in Q2, compared to a forecast of $13 billion last week. This is a very large change, and an important reason the model is forecasting such a strong quarter.

On top of that, data for capital goods shipments released last week was pretty strong, and advance inventory data was in line with the forecast. The shipments data is a key indicator that growth is likely to continue. At least for the time being, businesses are continuing to invest. I remain concerned about this being a bubble, and that, some time in the future, businesses will find themselves with a significant amount of excess capacity. If that happens, businesses will slash investment and hiring. But, for now, the boom is still on.

All three Fed forecasts, oddly enough, were revised down this week. They continue to remain very different, with the Atlanta Fed (like the Nowcast) pointing to near 4.0% growth, the St. Louis Fed at around 1.0%, and the New York Fed remaining in its very narrow range (currently it is 2.5%, and it generally moves in the range of 2.2% to 2.6%).