How I was wrong in Q1

And growth continues in Q2

The Nowcast returns! I just spent a lovely month in Europe, which has its own economic challenges. (But maybe not as bad as some people think: Paul Krugman’s very technical but insightful explanation of why productivity data may be misleading is well worth reading.)

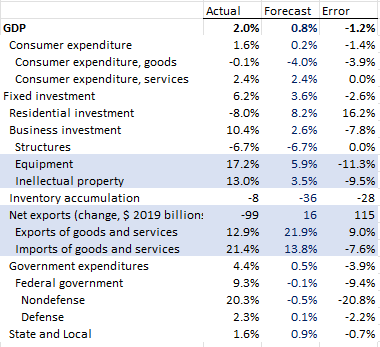

Back in the US, where GDP growth in Q1 surprised on the upside. A table shows the last Nowcast forecast for Q1 with the actual initial data:

The blue areas show the most interesting differences. Exports and imports were considerably higher than predicted; the March trade data showed much larger growth in both. In particular, imports of capital goods were up 15% (in nominal terms) in Q1 over Q4. That’s a huge jump in a category that ends up in equipment investment.

Which leads to the other set of differences. Equipment investment was up 17% (compared to the predicted 5.9%). The model depends on domestic shipments of equipment, so didn’t see the huge increase in imports (likely computer chips).

The picture is wholly consistent with the AI investment boom: a big jump in equipment partially in the form of imported chips, and a big jump in intellectual property investment despite declining employment in software. The decline in structures investment (both residential and non-residential) is a bit puzzling. I would expect this because of the shortage of construction workers, but the monthly data, particularly on housing starts, hasn’t show this. Although it’s possible builders are starting construction but taking longer to complete it.

The miss on government is to be expected; Q1 included a reverse of the Q4 decline because of the government shut down, and the model doesn’t pick up the BEA methodology correctly.

These misses added up to a broader miss in the overall picture of the economy. The Nowcast suggested that the economy was slowing. But the actual data confirm continued growth. It’s investment led, as consumer spending does indeed seem to be slowing, and on a narrow base involving AI investment, which is worrying.

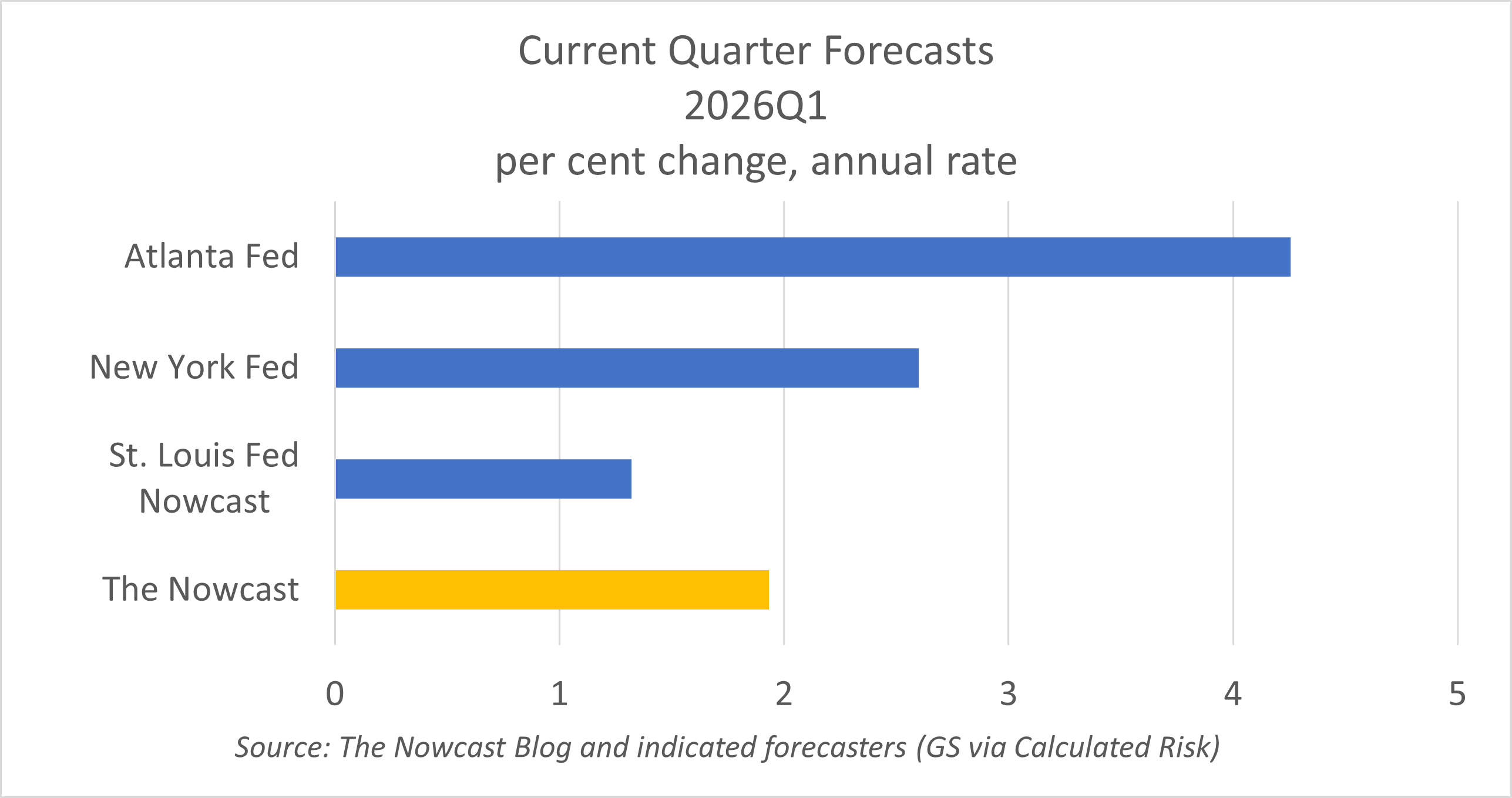

First look at Q2

The model is predicting continued growth at 1.9% in Q2. If this happens, it willb e quite impressive, given the massive volatility in the economic background, and the rise in fuel prices. At this point, the model points to most sectors of the economy reverting to something like their long-term growth rate. It’s a very vanilla sort of forecast. And we did get real consumer spending growing in March at 2.4%, which is quite good considering the rise in fuel prices. But it seems unlikely this will continue unless the Iran problem is solved and oil prices fall back to a reasonable level.