Down a little more

And why the Atlanta Fed is more optimistic

It’s all in the trade numbers.

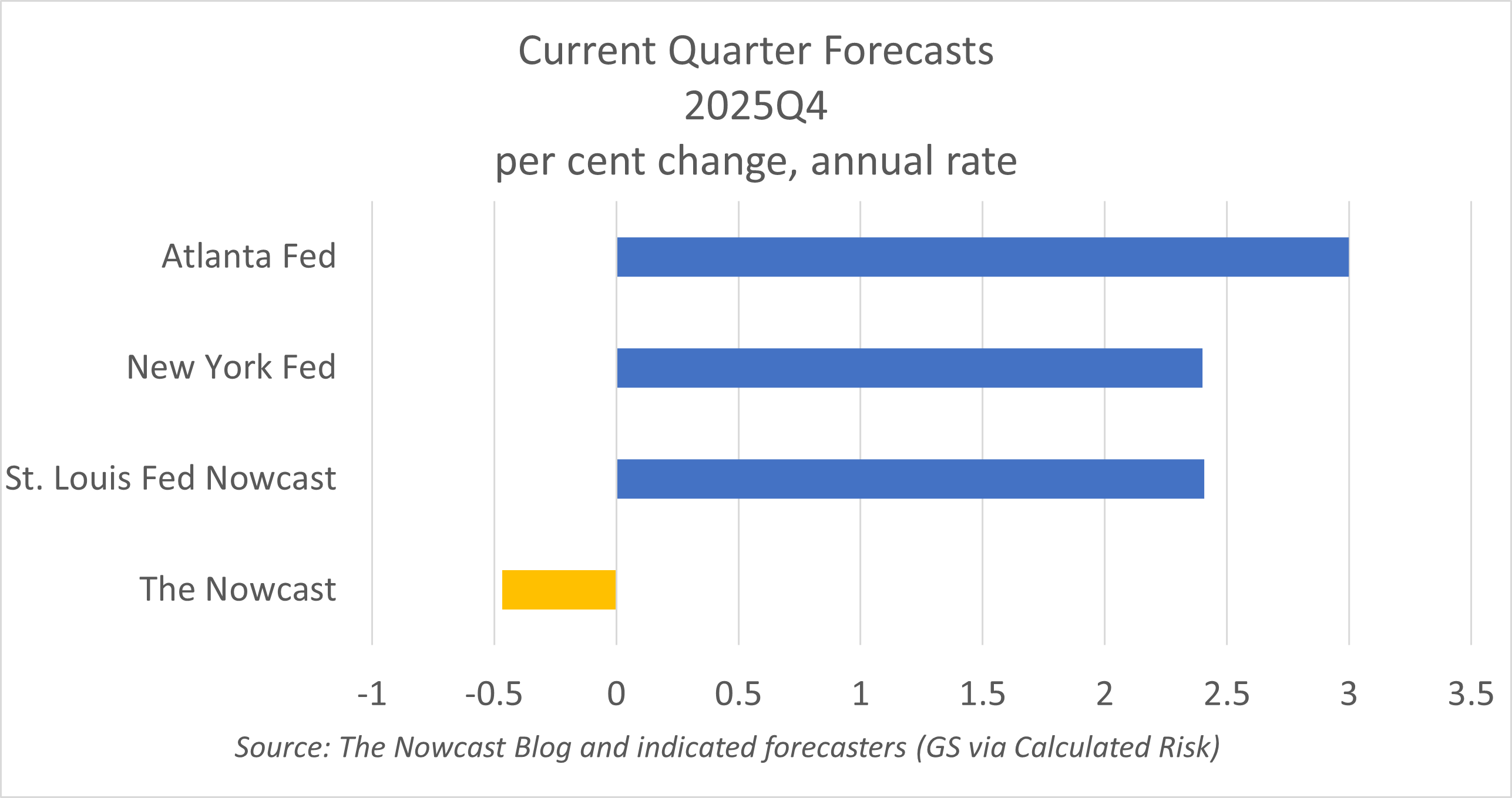

First, let’s just look at the possibility that GDP will be negative in Q1. That’s the Nowcast model forecast, although there are a couple of reasons to think it’s too pessimistic. But the possibility is out there. It doesn’t necessarily mean that the economy is about to go into a downturn, but it’s a sign that not everything is lining up perfectly.

The main new data this week was the updated construction spending data. With Census finally filling in the November and December data, we have a better look at where we left the end of the third quarter. It wasn’t positive, although it didn’t change the forecast that much. Real residential investment is forecast to grow 2.6% in Q1, compared to 3.3% last week, and real nonresidential construction investment is forecast to fall 7.7%, compared to 7.4% last week. That follows from a decline in nonresidential construction since September that the model expects to continue. (And manufacturing construction peaked in November 2024, and has been declining since—not a great sign for future manufacturing activity).

The model also pushed inventories and government down a bit. Together, all of these pushed GDP down two tenths of a percentage point, a small amount but definitely the wrong direction. However, much of the decline is due to the extreme drop in exports (8.3%) and even larger increase in imports (21.2%) projected by the model. These numbers are probably exaggerated because there is no adjustment for precious metals for investment (trade which does not count for GDP). Also, the government figures don’t take into account a rebound that will show up in the Q1 data, as the Federal government will have been operating for all three months at full scale, compared to the lack of production during the shut down period in Q4.

The Atlanta Fed’s GDPNow model is much more optimistic than the Nowcast. So are the St. Louis Fed and New York Fed models, although it’s impossible to understand why those models differ. In the cast of the Atlanta Fed’s model, I can compare the components and see that the Atlanta Fed has a large rise in exports (compared to the decline in the Nowcast) and a much more moderate increase in imports. Of course, “moderate” is a relative term here: the Atlanta Fed is forecasting an 8.7% rise in real imports, less than the Nowcast's 21.2% but still a very heft rise in imports.

I would guess that GDP is more likely to be in the 1% to 2% range for Q1, rather than the pessimistic model prediction of a decline. Consumer spending and private investment remain reasonably strong. But I wouldn’t rule a negative quarter out completely.